Coast FIRE With XEQT: How Much You Need Invested by Each Age

May 3, 2026

Coast FIRE is the most underrated version of financial independence. It does not ask you to retire tomorrow, grind to a seven-figure portfolio, or dramatically change your lifestyle. It asks one question: how much do you need invested right now so that, if you never added another dollar, compound growth would carry you to a comfortable retirement on its own?

The answer is smaller than you think. And XEQT, the iShares Core Equity ETF Portfolio, is one of the most efficient vehicles to get there.

What Coast FIRE Actually Means

The “coasting” part is the key. Once you hit your Coast FIRE number, you can theoretically stop contributing to your investments and let the market do the work. You still need to cover your current living expenses, so you are not retired yet. But you have permanently removed the pressure to save for retirement. Your paycheque becomes yours to spend, or to use however you want, without guilt.

This is why Coast FIRE resonates so strongly with Millennials and Gen Z. Full FIRE feels impossible when housing costs what it costs and real wages have been stagnant. But Coast FIRE feels achievable. You are not trying to retire at 35. You are trying to reach a number where your future self is taken care of, so your present self has more breathing room.

Coast FIRE does not mean you stop working. It means you stop working for retirement. Every dollar you earn after hitting your number is yours to deploy however you choose.

The math depends on three inputs: your target retirement number, your expected rate of return, and how many years you have for the money to grow. Change any of these and your Coast number shifts. But we can build a useful framework using reasonable, evidence-grounded assumptions for Canadians.

The Assumptions Behind These Numbers

Before presenting any figures, the assumptions need to be stated clearly, because garbage inputs produce garbage outputs.

For the retirement target, a common starting point is 25 times your expected annual spending, drawn from the 4% rule. Research from William Bengen and later the Trinity Study suggests a 4% annual withdrawal rate has historically survived 30-year retirements across most market environments. For a Canadian retiring with $50,000 in annual spending needs, that implies a portfolio of $1,250,000. This is conservative for a 30-year retirement and may need adjustment for a very early retirement, but it works well as a baseline for traditional retirement ages.

For the growth rate, XEQT holds approximately 9,500 stocks across global markets, weighted toward North America. Historically, a globally diversified equity portfolio has returned roughly 7% annually in real terms before fees. XEQT’s management expense ratio is 0.20%, leaving you with approximately 6.8% in real returns. For the Coast FIRE calculations below, a nominal return of 7% is used, which corresponds to roughly 5% real after a modest inflation assumption. Using real returns is more honest, since your retirement spending target should also be inflation-adjusted.

Key Assumptions: Retirement at age 65. Retirement spending target of $50,000/year in today’s dollars. Portfolio target: $1,250,000 (25x spending). Real return on XEQT: approximately 5% per year after inflation and fees. CPP and OAS not included, meaning these numbers are conservative for most Canadians.

One important note on CPP and OAS: these numbers intentionally ignore government benefits to be conservative. If you are entitled to CPP and OAS, your actual required portfolio could be significantly lower. A Canadian receiving $12,000/year from CPP and $8,000/year from OAS only needs their portfolio to cover $30,000 annually, reducing the target to $750,000. That makes your Coast number considerably smaller. Run your own numbers using the CPP Statement of Contributions available through your CRA My Account.

Coast FIRE Numbers by Age, Using XEQT

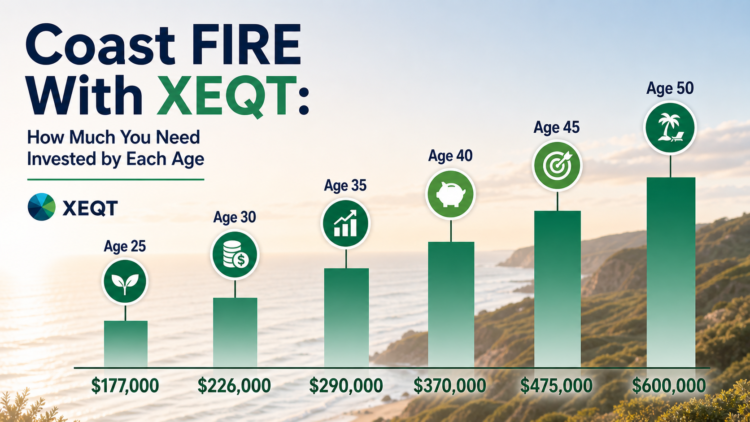

The following figures show how much you need invested in XEQT today to coast to a $1,250,000 retirement portfolio by age 65, assuming 5% real annual growth. Each figure is the lump sum that, left completely untouched, would grow to $1,250,000 by retirement.

Age 25: You have 40 years for your money to grow. At 5% real, your Coast number is approximately $177,000. That is an achievable target for a determined saver in their mid-twenties, especially using the TFSA and FHSA.

Age 30: With 35 years of compounding ahead, you need roughly $226,000 invested today. Still within reach for someone who has been consistently contributing since their early twenties.

Age 35: Twenty-five years to retirement means a Coast number of approximately $290,000. This is where many Millennials currently sit in the conversation. It feels large, but broken down into monthly contributions from age 22 onward, it is entirely realistic.

Age 40: The Coast number rises to around $370,000. The compounding runway is shorter, so the required upfront investment is larger. People who start investing seriously at 40 are not too late, but they have less margin for error.

Age 45: You need approximately $475,000 invested to coast from here to $1,250,000 by 65. This is where the math starts to feel punishing. The difference between reaching Coast FIRE at 35 versus 45 is nearly $185,000 in required capital, entirely because of a 10-year reduction in compounding time.

Age 50: With only 15 years left, your Coast number climbs to roughly $600,000. At this stage, most people are not coasting. They are still in full accumulation mode and likely will be for some time.

Every decade of delay roughly doubles the capital you need to reach your Coast number. This is not a motivational metaphor. It is compound interest working in reverse against you.

How to Get There: Account Priority for Coast FIRE in Canada

Once you understand your Coast number, the next question is which accounts to use to get there efficiently. Canada’s registered account system is genuinely excellent for this purpose, and using it correctly accelerates your timeline.

The TFSA is your first priority for Coast FIRE accumulation. The 2026 contribution limit is $7,000, and total room for someone who has been eligible since 2009 is now over $95,000. Growth inside a TFSA is completely tax-free, which means your 5% real return actually delivers 5% real, with no CRA involved at withdrawal. XEQT inside a TFSA is close to optimal.

The RRSP compounds your contributions with an upfront tax deduction. For most people earning above $50,000, the RRSP deduction generates a meaningful refund that can be reinvested, effectively boosting your real return. The contribution limit is 18% of prior year earned income, up to a maximum that adjusts annually. Use XEQT here too. One holding, total market exposure, no decisions required.

The FHSA is worth a specific mention for younger Canadians who have not yet bought a home. You can contribute $8,000 per year up to a $40,000 lifetime limit, with the same deduction benefit as an RRSP and the same tax-free withdrawal benefit as a TFSA if you use it for a first home purchase. If you end up not buying a home, unused FHSA room can be transferred to your RRSP without affecting your existing RRSP room. Either way, it is free tax shelter. Open it and fill it with XEQT.

Account Priority for Coast FIRE: TFSA first ($7,000/yr, tax-free growth and withdrawals). RRSP second (18% of income, deduction now, tax-deferred growth). FHSA if eligible ($8,000/yr, $40,000 lifetime, deductible and potentially tax-free). Non-registered account once registered room is exhausted.

Why XEQT Is the Right Vehicle for Coast FIRE

Coast FIRE’s entire logic depends on leaving money alone and letting it compound. That makes the vehicle choice more important than people realize. If you are going to be hands-off for 20 or 30 years, you need something that requires no maintenance, charges minimal fees, and holds its nerve through every market cycle without requiring you to hold yours.

XEQT holds four underlying iShares index funds covering Canadian equities, US equities, international developed markets, and emerging markets. The geographic diversification is automatic. The rebalancing is done for you. The MER is 0.20%, which means on a $300,000 portfolio you are paying $600 per year in fees. Compare that to the 1.5% to 2.5% charged by typical Canadian mutual funds, which would cost you $4,500 to $7,500 annually on the same balance. Over 30 years, that fee difference is not minor. It is portfolio-defining.

There is also the behavioural argument, which matters more than most people admit. Coast FIRE only works if you actually coast. If you are holding a collection of individual stocks or sector ETFs, you will be tempted to tinker. When tech sells off, you will wonder whether to rotate. When Canadian energy surges, you will wonder if you are underweight. XEQT eliminates the decision surface. There is nothing to tinker with. You own everything. You wait.

Wealthsimple and Questrade are both good platforms for holding XEQT in a TFSA or RRSP. Wealthsimple offers commission-free ETF trading and a clean interface that makes it easy to set up recurring purchases. Questrade offers free ETF buys with a slightly richer feature set for those who want it. Either one works. The platform matters far less than the consistency of your contributions.

The Honest Limitations of Coast FIRE Math

These numbers are models, not guarantees. A few things are worth keeping in mind before you declare yourself coasted and stop contributing.

Market returns are variable. A 5% real return is a long-run historical average, not an annual promise. XEQT will have years of 20% gains and years of 30% losses. The Coast FIRE math assumes you hold through both without panic-selling. If you cannot stomach watching a $300,000 portfolio drop to $210,000 on paper, you need to either adjust your risk tolerance or reconsider whether 100% equities is right for you during accumulation.

Sequence of returns risk matters less during accumulation than during withdrawal, but it still exists. Someone who hits their Coast number at 40 and then watches a brutal decade unfold between 40 and 50 may find they need to contribute more to stay on track. Checking your balance once a year against your updated projection is sensible. Obsessing over it monthly is not.

Life changes. Divorce, health issues, career breaks, supporting family members: all of these can alter the picture. Coast FIRE is a framework, not a contract. Treat the number as a milestone worth celebrating, not a finish line that releases you from all financial awareness.

The goal of Coast FIRE is not to think less about money. It is to worry less about it. Those are different things.

A Practical Path Forward

If you are in your twenties and reading this, the single most valuable thing you can do is open a TFSA at Wealthsimple or Questrade today, buy XEQT, set up an automatic monthly transfer, and then go live your life. You do not need a financial advisor to do this. You do not need a custom portfolio. You need consistency and time.

If you are in your thirties and have not started, start now. The Coast number at 35 is $290,000, which at $2,000 per month invested in XEQT from age 25 would have been reached around age 36 at historical average returns. If you are behind, you are not permanently behind. You just need to run the math on what monthly contribution gets you to your Coast number by what age, and then hold that target.

If you are in your forties and feeling like the window has closed, it has not. Coast FIRE at 45 requires $475,000, but full retirement savings at 65 with ongoing contributions is still very achievable. You may not get to coast in the pure sense, but you can still build a portfolio that gives you real options. XEQT is still the right vehicle.

The Canadian personal finance community talks endlessly about optimization: which ETF has the slightly lower MER, which brokerage has the fractionally better features, whether to hold XEF separately for foreign withholding tax reasons. Most of that is noise. The decision that moves the needle is whether you are invested at all, and whether you stay invested through volatility. XEQT solves the first problem by design. Your own behaviour solves the second.

Frequently Asked Questions

What is a realistic Coast FIRE number for the average Canadian? It depends on your retirement spending target and current age, but using $50,000 per year in today’s dollars as a spending target and assuming CPP and OAS will not cover everything, a reasonable range is $175,000 to $475,000 depending on whether you are 25 or 45. If you include expected CPP and OAS benefits, these numbers drop significantly for most Canadians.

Does XEQT work for Coast FIRE inside an RRSP as well as a TFSA? Yes. XEQT is appropriate inside any registered account. The TFSA is generally preferred for Coast FIRE because withdrawals are tax-free and do not affect income-tested benefits in retirement. But the RRSP is equally valid during accumulation, especially if your current marginal tax rate is higher than you expect it to be in retirement.

What if I want to retire before 65? If you are targeting a retirement age of 55 or 60, your Coast FIRE number gets significantly larger because the compounding runway is shorter and your drawdown period is longer. A 55-year-old retirement might require a portfolio of $1,500,000 or more, which raises the required Coast number at each age. Run the same calculation using your actual target retirement age rather than 65.

Should I switch to a more conservative ETF like XGRO once I hit my Coast number? This is a personal call, but the case for staying in XEQT is stronger than many people expect. If you are coasting for 20 or 30 years, you still have a very long time horizon. The volatility of 100% equities is most dangerous near or in retirement, not during a long coast phase. That said, as you approach within 5 to 10 years of your actual retirement date, gradually shifting toward a more balanced allocation is a reasonable move. You do not need to time it perfectly.